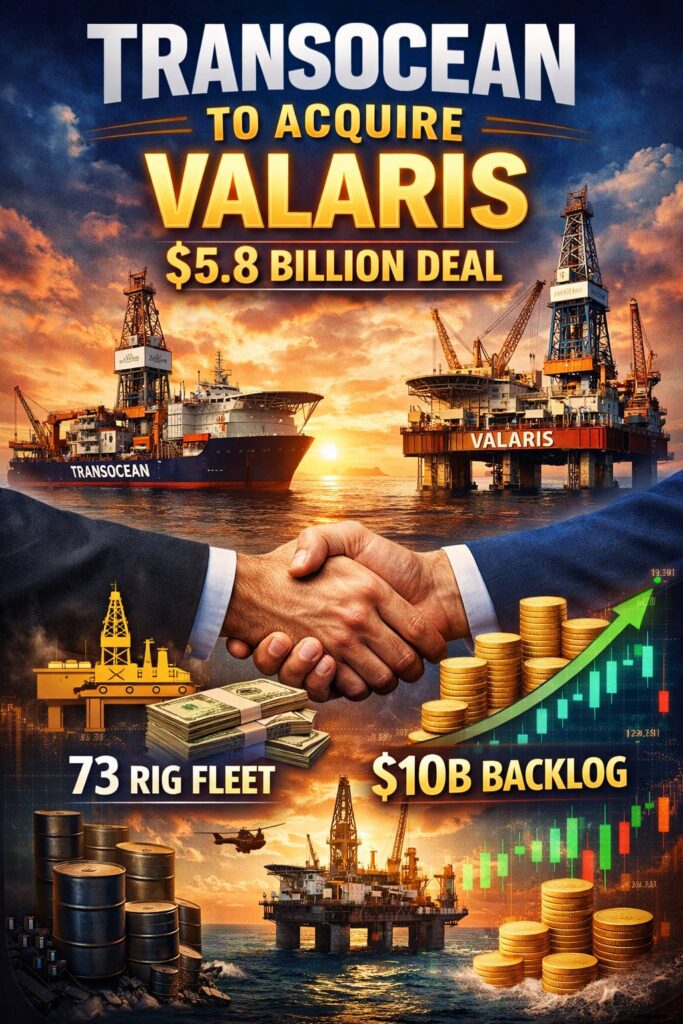

Transocean’s agreement to buy Valaris in an all-stock transaction valued around $5.8 billion is a classic late-cycle move: lock in scale while customers chase longer-dated offshore barrels, and sell a “bigger, steadier platform” story to investors who still remember how fast drilling cycles can turn. The combined operator would control 73 rigs across deepwater, harsh-environment, and shallow-water work—instantly shifting Transocean from a floater specialist to a full-spectrum offshore contractor.

The headline logic is easy to market: more rigs, broader customer coverage, and a thicker contract book. The harder part—and where the stock debate usually lives—is the trade-off between future cash-flow stability and near-term dilution plus integration risk. If management executes, the upside is a more resilient earnings profile and faster deleveraging. If dayrates soften or the integration drags, shareholders may feel they paid for “scale” with a higher share count and more moving parts.

What investors are actually buying: a re-rating attempt built on a single idea—customers prefer fewer, stronger contractors that can deliver multiple rig types across multiple basins. Transocean has historically been identified with high-spec floaters: ultra-deepwater drillships and harsh-environment semisubs that can command premium dayrates when the market tightens. Valaris adds a meaningful jackup footprint alongside additional deepwater capacity, turning the combined group into a one-stop bidder for tenders where operators want optionality: deepwater development today, jackup work tomorrow, and mobilization strength across regions.

How the fleet mix changes the story: floaters can be “higher beta”—bigger contract values, stronger margins in tight markets, but also sharper downside when utilization slips. Jackups tend to bring a different rhythm: shorter contract durations in many regions, more competition, and a pricing cycle that does not always move in lockstep with deepwater. That mix can smooth earnings in one scenario and complicate them in another. The market will likely focus on whether Transocean can avoid diluting its premium floater positioning while absorbing a large jackup business.

Synergies are the credibility test: management has pointed to more than $200 million in cost synergies, with the usual levers in this sector—shore-base consolidation, procurement, overlapping corporate functions, and tighter fleet deployment planning. Offshore drilling is operationally complex, but it’s also an industry where duplicated overhead can be surprisingly large when two global operators combine. The market will watch for concrete milestones: how quickly contracting teams are unified, whether stacked rigs can be rationalized, and whether utilization improves without sacrificing pricing.

Backlog is the “sleep at night” factor: the combined group is talking about roughly $10 billion of backlog—important because it’s the cleanest way to argue that a bigger fleet does not automatically mean a riskier fleet. Investors who have been reluctant to pay up for drillers often cite the same concern: the business can look great on dayrates—until contract coverage thins. If the combined backlog remains durable through 2026 and beyond, the equity pitch becomes simpler: steadier contracted revenue, steadier cash generation, and a clearer path to balance-sheet repair.

The shareholder trade-off, in plain English: because this is all stock, Valaris holders get a fixed exchange ratio and Transocean ends up with more shares outstanding. That dilution can be perfectly rational if it buys durable cash flows and accelerates deleveraging—but it also means the company must “earn back” the higher share count with synergy delivery, improved utilization, and strong contracting. In other words: the deal can work even without a blow-off boom in dayrates, but it can’t work with sloppy execution.

Three things that can move the stock narrative fast: first, the approval path—regulatory and shareholder sign-offs, and whether the targeted second-half 2026 close remains on track. Second, the synergy roadmap—timing, costs to achieve, and whether the savings show up in cash flow rather than slides. Third, contracting momentum—especially in deepwater basins like Brazil and in harsh-environment work where Transocean has been active, because premium floater utilization is still the “earnings engine” investors care about most.

For readers tracking offshore cyclicals, this merger is a reminder that the sector is trying to look more like a modern industrial business—fewer operators, bigger fleets, more contracted visibility, and a clearer capital-return story over time. Whether it gets rewarded like one will depend on execution and discipline, not just scale.

If you follow energy and industrial names closely, you can also browse more market coverage on Swikblog.

For the official transaction announcement details (terms, timing, and merger rationale), see the companies’ release here: Transocean to Acquire Valaris .

Disclosure: This article is for informational purposes only and is not financial advice.

Make Swikblog your go-to source on Google for reliable updates, smart insights, and daily trends.