Fri, 23 January 2026 • UK

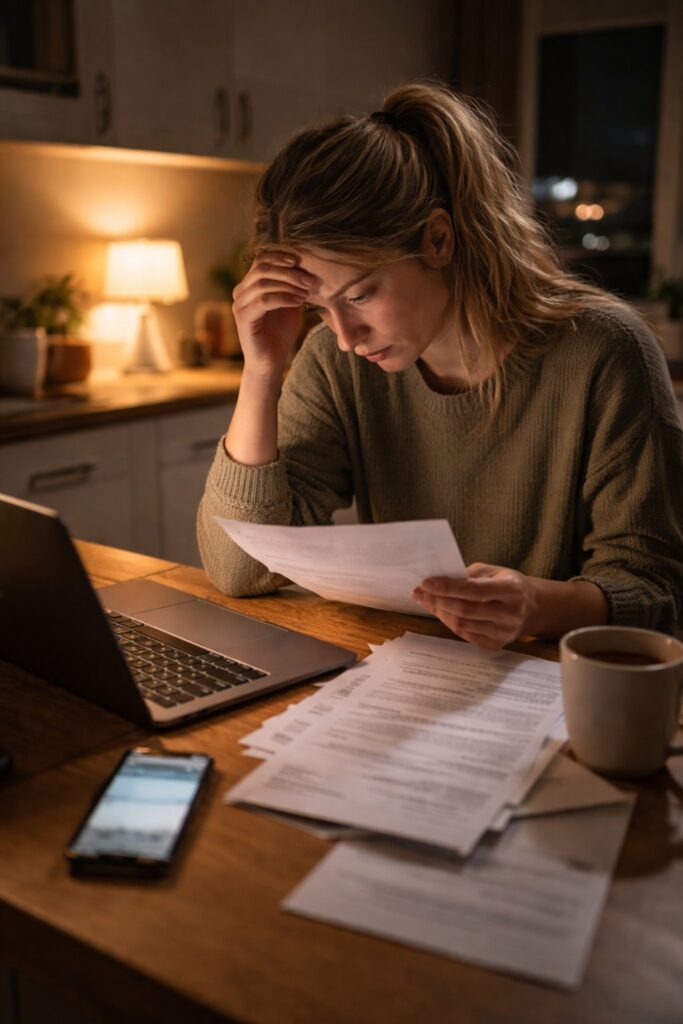

The message lands with a thud when you open your statement: you’ve been working, you’ve been paying, you’ve been “doing the right thing” — and the balance is higher than the last time you looked. For a growing number of UK graduates, that moment isn’t just frustrating. It’s destabilising, like discovering the rules of the game were different all along.

Part of the shock comes from what we’ve been trained to expect. A normal loan shrinks when you repay it. With UK student loans, many graduates are finding the opposite: repayments arrive like clockwork, yet the total can move sideways for years, or climb. It feels like running on a treadmill that quietly speeds up when you’re not looking.

What graduates are bumping into isn’t personal failure. It’s the maths of a system where interest can outpace repayments for long stretches of time.

Start with how repayments work in real life. Most people don’t write a cheque each month; the money is taken automatically through payroll once earnings pass a threshold for their plan. That can make the whole thing feel distant, almost invisible — until you check the balance. The deduction looks manageable, so the assumption is the debt must be falling too. But the balance is doing its own thing in the background.

The key reason is interest. UK student loans don’t behave like a typical bank loan where rates are purely market-driven and the borrower steadily chips away at the principal. Instead, interest is structured in a way that can keep the balance elevated for years, particularly for people whose earnings don’t rocket upward early in their careers. When your annual repayments are smaller than the interest being added, the balance won’t shrink — and can rise.

That dynamic hits hardest in the years when graduates are trying to build a life at the same time as everything else is getting pricier: rent, commuting, childcare, food, energy. Student loan deductions can feel like one more quiet tax on the payslip, except it doesn’t come with a clear finish line. The balance becomes less like “debt you’ll clear” and more like a long-term obligation you live alongside.

Another part of the confusion is psychological. We talk about “debt” and “repayment” in a way that suggests a clean endpoint — but many graduates won’t see that. The system includes a write-off point after a certain number of years, depending on the plan, which means plenty of borrowers repay for a long time without ever clearing the full balance. For them, the number on the statement can start to feel symbolic rather than practical: huge, intimidating, and not necessarily linked to what they’ll actually pay over a lifetime.

If your balance seems to rise even while you repay: it usually means interest is accumulating faster than your repayments at your current income level, especially in the early and middle years after graduation. Your repayments are still counting — they’re just not reducing the headline figure yet.

This is where the “only now finding out” part comes in. Many graduates simply weren’t tracking their loan closely because the repayment method makes it easy not to. Others assumed it would behave like other borrowing. And some were told, bluntly, not to worry about it — as if ignoring it was the healthiest financial strategy. That advice made emotional sense at the time. In 2026, it’s colliding with the reality of squeezed wages and stubbornly high costs.

So what can you do — realistically — if you’re staring at a balance that won’t budge? First, understand your plan and the rules you’re on, because the details matter: thresholds, interest structure, and the write-off timeframe all shape how repayments feel. The most reliable place to check the official mechanics is the government’s guidance on repaying your student loan, which lays out how deductions work and where to manage your account.

Second, try not to let the headline balance hijack your entire financial life. For many graduates, the student loan behaves more like a long-term payroll deduction than a debt you should attack at all costs. Overpaying can make sense for some high earners in certain circumstances, but it can also be the wrong move if it diverts money away from emergency savings, housing stability, or pension contributions. The right decision is rarely emotional — even if the statement makes it feel personal.

And finally, talk about it. One reason the system shocks people is the silence around it: friends compare rent, not loan plans; families remember grants, not modern repayment rules; workplaces avoid the subject entirely. But the more openly graduates share what they’re seeing, the harder it becomes to pretend that a swelling balance is a rare glitch instead of a widespread feature.

If you’re one of the many graduates paying regularly and still watching the number climb, you’re not imagining it. You’re seeing the system as it operates — and you’re far from alone. For a whole generation, the real cost of a degree isn’t only what was paid upfront. It’s the years of deductions that follow, and the uneasy feeling that repayment doesn’t always mean relief.

For more UK explainers and updates you can share, browse our coverage here: student loans on Swikblog.

Make Swikblog your go-to source on Google for reliable updates, smart insights, and daily trends.