Oscar Health is trading higher before the opening bell after posting mixed fourth-quarter results, with investors weighing revenue momentum, cash flow and a renewed push toward profitability.

Oscar Health’s latest earnings sharpen the tug-of-war driving OSCR. The insurer missed Wall Street expectations on both profit and revenue, but paired the weak quarter with an eye-catching 2026 outlook that’s pushing investors to weigh forward momentum against current cost pressure.

Oscar reported fourth-quarter EPS of -$1.24, about $0.35 worse than the -$0.89 analyst estimate, while revenue came in at $2.81B versus roughly $3.11B expected.

Guidance is the headline: Oscar now sees FY 2026 revenue of $18.70B–$19.00B, far above the $12.76B consensus. Shares closed at $12.67, down 9.18% over three months and 10.21% over the past year, even as estimate changes have tilted positive with five upward versus two downward EPS revisions in the last 90 days.

Last close

$12.66 +3.43%

Previous close: $12.24

Pre-market

$13.35 +5.37%

Bid $12.95 · Ask $13.08

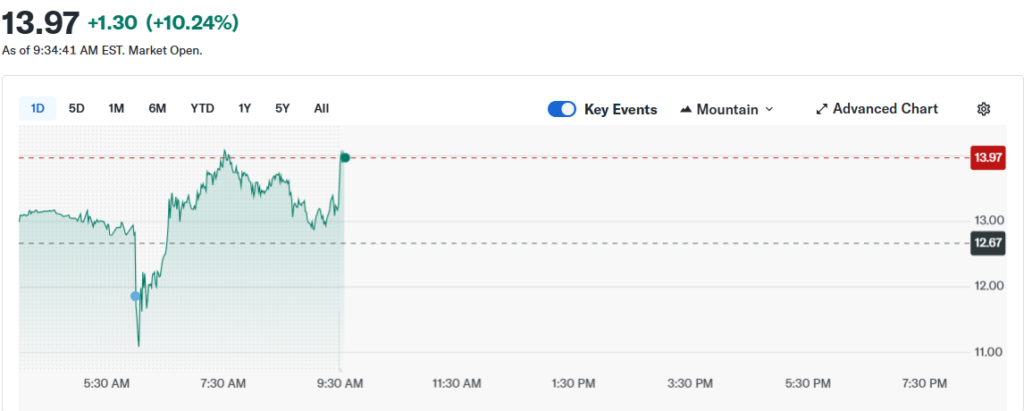

Oscar Health’s pre-market pop is the kind of move that usually comes with a clean earnings beat. This one is messier: the insurer reported a wider fourth-quarter loss and missed consensus revenue expectations, yet the stock is trading higher before the bell. The explanation sits in what traders are choosing to emphasize today, and what they are willing to discount.

Start with the headline tension. On one hand, the company’s quarterly results highlighted pressure from elevated healthcare utilization, the sort of trend that can squeeze margins quickly for insurers. On the other, Oscar Health’s revenue grew year over year, cash generation improved, and management reiterated a determined shift toward profitability in 2026. In pre-market trading, it’s the forward narrative that tends to win the first round.

Earnings snapshot: the numbers investors are reacting to

Revenue

$2.81B, up 17.3% year over year

Revenue vs expectations

Missed estimate of $3.12B

GAAP EPS

-$1.24 per share

EPS vs expectations

Below estimate of -$0.86

Adjusted EBITDA

-$307.8M, about -11% margin

Operating margin

-11.9%, down from -6.2% a year ago

Free cash flow margin

23.6%, up from 14.2% a year ago

2026 view

Management says profitability is the goal

The market is treating guidance and cash flow improvement as “directional” signals, even while the loss line widened in Q4.

So why is OSCR up if the quarter looked soft? Pre-market trading often compresses a complex earnings package into a few decisive themes. For Oscar, the bullish read is that 2025 was positioned as a reset year and that actions taken across pricing, risk management and operating focus are meant to show up in 2026 results. That storyline has an obvious trading appeal: if the market believes losses can narrow meaningfully, the valuation can re-rate quickly from depressed levels.

The bears, however, will keep coming back to utilization and medical cost pressure. For insurers, sustained spikes in medical spending can overwhelm premium growth and erode profitability targets. The quarter’s wider loss is a reminder that the model still has to prove it can hold margins when members use more care than expected. If claims trends stay hot, the path to profitability becomes longer, and the stock’s pre-market optimism can evaporate just as quickly as it arrived.

What traders will watch after the open is whether the pre-market bid holds once liquidity arrives. The stock is already trading above its prior close, and pre-market levels near the mid-$13s put it closer to a zone where intraday profit-taking often shows up, especially after an earnings catalyst. If buyers keep stepping in on dips, the tape will likely be signaling that the market is prioritizing forward guidance and cash durability over the quarter’s ugly loss figure.

Two practical levels matter in the very near term. First is the prior close region, because a move that can stay above that line often suggests the market is “accepting” the post-earnings repricing. Second is the pre-market high zone, because that becomes the first real test of conviction: if the stock can’t clear it, traders may fade the move; if it breaks and holds, momentum funds can pile in.

If you’re building a longer-term view, the lens shifts from today’s spike to 2026 execution. The market is effectively asking one question: can Oscar Health translate growth into durable profitability without getting blindsided by claims volatility? Investors looking for the company’s official filings, results materials and forward commentary can follow updates directly via Oscar Health investor relations.

You may also like: Follow more market movers and earnings reactions on Swikblog.

Make Swikblog your go-to source on Google for reliable updates, smart insights, and daily trends.