Premium Bonds holders are getting a summer boost from NS&I, but savers hoping for another prize rate rise later in 2026 may need to watch interest rates, Government funding targets and how quickly money flows into NS&I products.

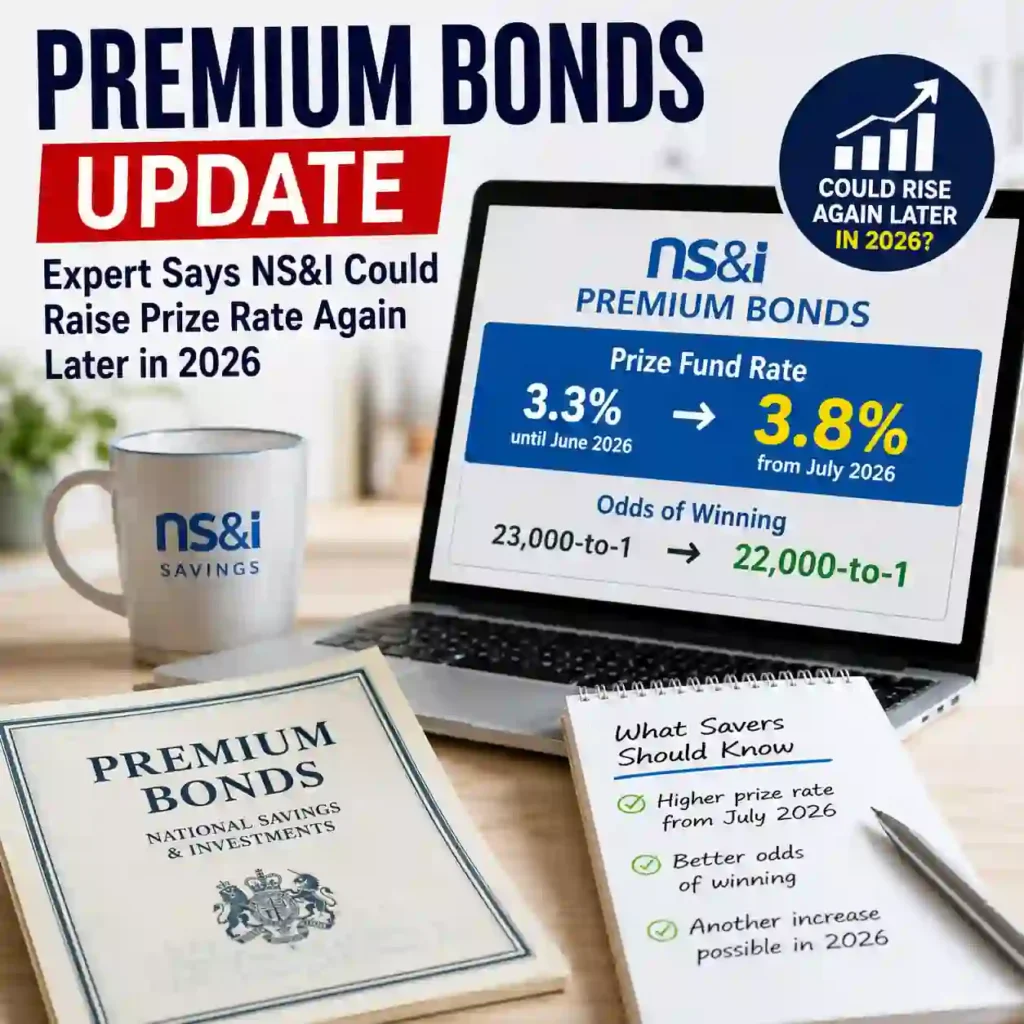

The confirmed change starts with the July 2026 Premium Bonds draw. NS&I is raising the prize fund rate from 3.3% to 3.8%, while the odds of each £1 Bond winning a prize improve from 23,000-to-1 to 22,000-to-1. The update affects more than 22 million Premium Bonds holders and comes after NS&I also lifted rates on several fixed-term savings products.

The important detail for savers is that the July increase is confirmed, but another increase later in the year is not. Experts say further movement is possible if the UK savings market remains competitive, but NS&I’s role as a Government-backed savings provider makes the decision more complicated than a simple rate race.

Premium Bonds are getting a confirmed July boost

From the July draw, the Premium Bonds prize fund rate will rise to 3.8%. That is up from the 3.3% rate that applied after earlier changes in 2026.

The prize fund rate is not the same as a normal savings interest rate. Premium Bonds do not pay fixed monthly interest. Instead, the rate is used to calculate the overall prize fund available in the monthly draw. Some holders may win more than the headline rate suggests, while others may win nothing.

NS&I says the July change will shorten the odds of winning to 22,000-to-1 for each £1 Bond held. The official NS&I Premium Bonds announcement also says the change is expected to add around 322,000 extra prizes each month compared with May 2026, taking the monthly prize fund to about £436.8 million.

Why another prize rate increase is being discussed

The question of another increase has come up because NS&I has not only improved Premium Bonds. It has also raised rates across other savings products, including British Savings Bonds and Green Savings Bonds.

That wider move suggests NS&I is responding to conditions in the savings market. When banks and building societies offer stronger rates, NS&I has to consider whether its own products remain attractive enough to meet its funding needs.

Premium Bonds are especially sensitive to this comparison because they offer chance rather than certainty. A saver choosing a fixed-rate bond knows the interest rate they will receive. A Premium Bonds holder gets monthly prize draw entries, but no guaranteed return.

Expert outlook depends on Bank of England rates

George Sweeney, investing expert at Finder, said future changes to the Premium Bonds prize rate are possible, but difficult to predict. Bank of England base rate decisions will be one factor, particularly if the market continues to expect rates to remain higher for longer.

If savings rates stay elevated across the wider market, NS&I may have more reason to keep Premium Bonds competitive. A higher prize fund rate could help retain existing holders and attract new money from savers looking for tax-free prizes and Government-backed security.

But the link is not automatic. NS&I does not operate like a normal commercial bank. Its purpose is not simply to chase deposits or maximise profit. It raises money for the Government while offering savings products to the public.

NS&I’s £15 billion financing target matters

A key part of the story is NS&I’s net financing target. For the 2026/27 tax year, the Government has set NS&I a target of £15 billion.

That target changes how savers should read the latest update. NS&I needs to raise money for the Treasury, but it also has to avoid raising too much. If the July Premium Bonds boost and the new fixed-term rates bring in funds faster than expected, another prize fund increase may become less likely.

In simple terms, a higher Premium Bonds prize rate can attract more money. That helps if NS&I needs stronger inflows. But if it is already on track, raising the prize rate again could make the product more generous than necessary for its Government mandate.

Full list of NS&I rate changes

NS&I’s latest savings update included several fixed-term rate rises announced in June. The new rates include:

- Guaranteed Growth Bonds 1-year: 4.69%, up from 4.50%

- Guaranteed Income Bonds 1-year: 4.69%, up from 4.50%

- Guaranteed Growth Bonds 2-year: 4.67%, up from 4.48%

- Guaranteed Income Bonds 2-year: 4.67%, up from 4.48%

- Guaranteed Growth Bonds 3-year: 4.65%, up from 4.45%

- Guaranteed Income Bonds 3-year: 4.69%, up from 4.45%

- Guaranteed Growth Bonds 5-year: 4.55%, up from 4.40%

- Guaranteed Income Bonds 5-year: 4.55%, up from 4.40%

- Green Savings Bonds 3-year: 4.45%, up from 3.82%

The Green Savings Bond has a separate purpose because it was introduced to help finance green Government projects across the UK. That makes it different from products that directly feed into NS&I’s main net financing target.

What it means for Premium Bonds holders

For existing holders, the July change is positive because the prize pot is larger and the odds are better. However, it does not mean every saver will earn 3.8% on their money.

The more Bonds someone holds, the more entries they have in the monthly draw. But Premium Bonds still rely on probability. A person with a large holding may win several prizes, while another saver with the same amount may receive nothing over the same period.

This is why Premium Bonds are usually more attractive to savers who value tax-free prizes, easy access and Treasury backing, rather than those who need predictable interest income.

For readers comparing this update with other UK savings changes, our earlier report on the Premium Bonds prize rate rising to 3.8% and improved NS&I winning odds explains the confirmed July draw changes in more detail.

Read More

Premium Bonds versus fixed savings accounts

The biggest difference between Premium Bonds and fixed savings accounts is certainty. Fixed-rate products show savers exactly what return they will receive if they keep money invested for the full term. Premium Bonds offer flexibility and a chance of winning, but the outcome is uncertain.

That distinction matters more when fixed savings rates are high. If a saver wants guaranteed income, a fixed-rate bond or cash ISA may be easier to plan around. If a saver has already used tax-free options or prefers the chance of larger prizes, Premium Bonds may still fit their needs.

Inflation is another factor. If a Premium Bonds holder wins nothing, the real value of their savings can fall over time as prices rise. That risk is easy to overlook because the product is Government-backed, but capital safety does not mean guaranteed growth.

What savers should watch later this year

The next signal will come from the Bank of England’s interest rate path. If rates stay higher for longer, savings competition may remain strong, making another NS&I adjustment more likely.

The second signal is NS&I’s fundraising progress. If it needs more money to stay on track for its £15 billion target, improving Premium Bonds again could be an option. If it raises funds quickly, the pressure to offer another prize rate boost may ease.

The third factor is customer behaviour. Strong demand for the July Premium Bonds draw and the new fixed-term savings rates could reduce the need for further action.

For now, Premium Bonds holders have a confirmed improvement from July: a 3.8% prize fund rate, better 22,000-to-1 odds and a larger monthly prize pool. Another increase later in 2026 remains possible, but it is an outlook rather than an announcement.

Make Swikblog your go-to source on Google for reliable updates, smart insights, and daily trends.